Have you ever found yourself caught up in a burst of motivation, determined to overhaul your finances overnight? Meet Sarah, a marketing professional who started 2023 with $27,000 in credit card debt. Like many of us, she began with an ambitious plan to eliminate all her debt in just six months through extreme budgeting. But as she—and countless others—have discovered, achieving financial success isn't about those rare bursts of extreme effort. It's about making consistent, intentional choices that align with your long-term goals.

Identity-Based Habits vs. Outcome-Based Goals

James Clear, author of "Atomic Habits," reveals a striking statistic: 45% of our daily activities are habits, not decisions. Yet when setting financial goals, many people focus on outcome-based goals, such as saving $10,000 for an emergency fund or paying off all their debt. While these goals are important, they can sometimes feel daunting and out of reach, especially if you're just starting your financial journey. Instead, consider focusing on identity-based habits—the small, consistent actions that align with the person you want to become.

Consider Michael's story. Fresh out of college, he felt overwhelmed by financial advice suggesting he needed to save 20% of his income for retirement. His solution? Starting with just enough to get his company's 3% 401(k) match—about $50 per paycheck. What seems almost too small to matter to most, but by creating this system that $50 became automatic, just another line item in his budget. Today, ten years later, his retirement account has grown to six figures, built primarily through small, consistent contributions and compound growth.

The Procrastination Test: When "Someday" Means "Never"

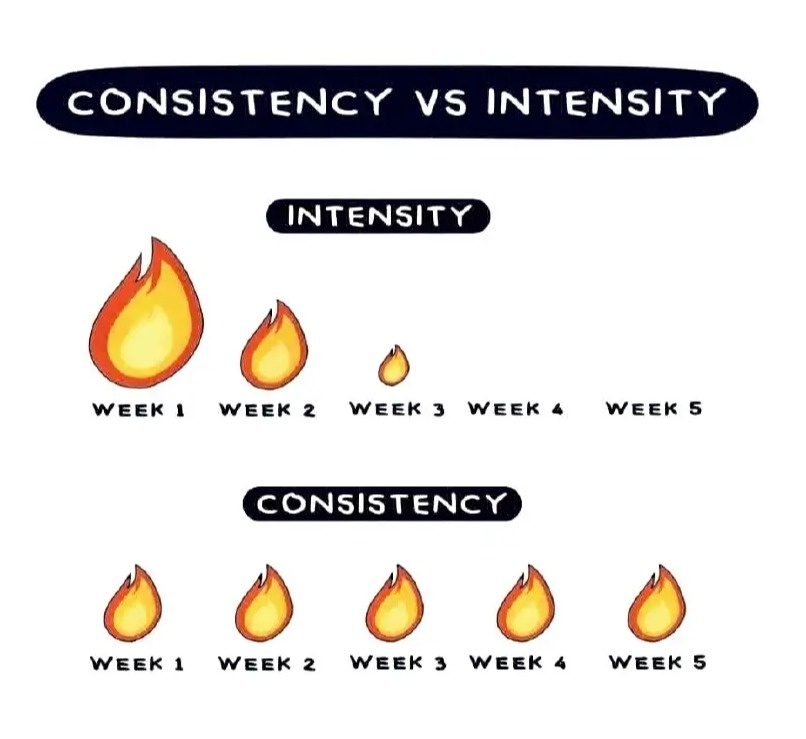

Research shows that only 9% of New Year's resolutions succeed. But those that do share a common thread: they're built on small, consistent actions rather than dramatic changes.

Here's a powerful truth about goals: if it's not important enough to start today, it might not be important enough to do at all. When you find yourself procrastinating, it usually signals one of two things: either the goal isn't truly aligned with your priorities, or your system needs adjustment.

Consider fitness goals. If you're consistently putting off going to the gym for hour-long workouts, the issue might not be the goal itself, but rather the system you've designed. Starting with a more manageable commitment—like a 20-minute daily walk—creates momentum through consistency. The same applies to financial goals: if saving $500 monthly feels overwhelming, start with $50 automatic transfers.

Take Tom's story. For years, he talked about wanting to build an emergency fund. Mentioning things about starting after a raise or the holidays. But when he finally got honest with himself, he realized that if financial security was truly a priority, he needed to start immediately—even if that meant just $25 a week. The day he made this mental shift was the day his relationship with money began to change.

The Reality of Trade-offs and Big Picture Thinking

Every financial goal you prioritize comes with trade-offs—there is no free lunch. The Martinez family discovered this when they opted for local weekend trips rather than expensive vacations, building their emergency fund while still creating family memories. Emma chose to drive her paid-off car for an extra three years, directing the would-be car payments to her retirement savings instead.

However, here's the encouraging part: improvements in one financial area often create unexpected benefits in others. When Sarah eliminated her credit card debt through the snowball method, she found herself sleeping better at night. Michael's small 401(k) contributions taught him budgeting skills that helped him save for a house down payment. The Martinez family's local adventures helped them discover a passion for hiking that improved their health.

Building Systems That Support Your Desired Financial Identity

Successful individuals create systems that align with their financial identity. This means automating savings, setting up direct payments for bills, and structuring budgets that reflect their values. Sarah's breakthrough came when she stopped relying on willpower and instead automated her debt snowball payments, ensuring that extra $200 went to her smallest debt automatically each month.

The $100/Month Example: Small Actions, Big Identity Shifts

Imagine setting aside just $100 a month towards a specific financial goal. While $100 may not seem significant at first glance, it represents more than just the money saved—it's a vote for your future self. For the Martinez family, their modest $100 weekly savings eventually grew into a robust emergency fund that gave them peace of mind during an unexpected job transition.

Understanding the Timeline of Change

Success isn't about doing more -- it's about doing less, but better. Just as the most successful athletes focus on fundamental movements rather than flashy techniques, financial success comes from mastering basic habits rather than finding "secret" strategies.

Here's something rarely discussed about meaningful financial goals: they almost always take longer than we expect. Most sustainable changes take 18-24 months, not weeks. Sarah didn't eliminate her $27,000 in debt overnight—it took her two years of consistent effort. But by accepting this timeline from the start, she maintained her motivation even when progress seemed slow.

Action Steps to Align Today's Decisions with Tomorrow's Identity

- Choose Your Small Win: Pick one financial goal that's important enough to start today—not tomorrow, not next week. Remember, if it's not worth starting now, it might not be a true priority.

- Identify Trade-offs: Be honest about what you'll need to say "no" to, like the Martinez family choosing local adventures over expensive vacations.

- Create Automatic Systems: Set up systems that work while you sleep, whether it's auto-drafting $100 to savings or using apps to track spending.

- Accept the Timeline: Most meaningful financial changes take 18-24 months. Plan for the long game.

- Track Your Progress: Create a simple way to monitor your journey, like Sarah's debt thermometer on her fridge.

- Look for Ripple Effects: Notice how improvements in your finances positively impact other areas of your life.

- Start Today: Because if a goal is truly important, there's no better time than right now.

Conclusion

Remember, every financial success story starts with a single step, maintained consistently over time. Sarah didn't eliminate her debt overnight. Michael didn't build his retirement savings in a month. The Martinez family didn't create their emergency fund in a week. But through small, consistent actions, they all achieved goals that initially seemed out of reach.

Your journey to financial success isn't about dramatic gestures or extreme sacrifices. It's about making small, intentional choices every day that align with your long-term vision.

Your Next Step: Open your banking app right now. Set up an automatic transfer—even if it's just $25—to start today. Don't wait for the "perfect" amount or the "right" time. Choose one small financial action that you can maintain consistently and take that step before you close this article. Remember, heroic consistency beats heroic effort every time.

Ready to start your journey toward financial success? We are here to help. Contact our team of financial advisors to create your personalized plan for building lasting wealth through consistent action. Email us at info@aperionplanning.com to schedule your free consultation.

Sources:

- "The 45% of Daily Behaviors That Are Habits," James Clear, Atomic Habits

- "Why Only 9% of People Keep Their New Year's Resolutions," Discover Happy Habits

- "The 18-24 Month Timeline for Sustainable Change," ACE Fitness